Agentic AI in banking is shifting institutions from manual, operations-heavy workflows to systems that can actually act and execute tasks independently. Yet, banks still spend 50–60% of workforce capacity on service operations, driving costs and slowing decisions.

Estimates from McKinsey & Company suggest agentic AI could reduce banking operation costs by 15–20%, while BCG projects up to 30–40% lower costs and 30% higher profitability by 2030.

However, despite this strong business case, adoption is still limited with only about one-third of organizations scaling AI beyond early experiments, while others remain stuck in what McKinsey calls “pilot purgatory.”

Dextra Labs designs and deploys AI agents for finance across regulated markets in India, USA, Singapore and UAE. With expertise in enterprise AI and compliant data systems, Dextra Labs helps financial institutions move beyond early experiments to scalable, production-ready systems. In this blog, we’ll discuss how to implement agentic AI in banking, explore key use cases, break down the architecture and explain how you can move from pilot to production. Let’s begin the guide!

What is Agentic AI in Banking?

Agentic AI in banking refers to smart systems that can plan, make decisions and take actions to achieve specific goals across banking workflows. Unlike traditional AI, which focuses on single tasks or predictions, agentic AI combines reasoning, memory and tool usage to execute end-to-end processes.

These agents can interact with multiple banking systems, access real-time data and adapt their actions based on outcomes, whether it’s processing loan applications, detecting fraud patterns, or handling compliance checks. By operating with minimal human intervention, they enable banks to move from task-based automation to fully coordinated, goal-driven workflows.

Why Agentic AI Is Becoming Mission-Critical for Banks (2026 and Beyond)

Banks are facing a sharp rise in transaction volumes and operational complexity. In fact, as per Statista survey, the total digital payment transaction value is expected to grow at a 7.63% CAGR from 2026 to 2030, reaching $36.09 trillion by 2030. This growing scale makes it increasingly important for banks to adopt agentic AI to modernize as well as automate their core operations effectively.

Also, as transaction volumes grow, the scale and sophistication of risks increase alongside them.

Fraud is evolving faster than traditional controls. Juniper research estimates that global online payment fraud losses could surpass $362 billion between 2023 and 2028, highlighting the limits of rule-based detection systems.

This is where agentic AI in banking becomes so important. Unlike static automation, AI agents in banking can independently analyze signals, take actions and adapt in real time which makes them well-suited for dynamic financial environments.

Why banks are accelerating adoption now:

- Rising transaction volumes: Scaling operations manually is no longer sustainable at projected growth levels.

- Increasing fraud sophistication: Static rules struggle, while agentic systems continuously learn and respond.

- Operational efficiency pressure: Banks are adopting automation to reduce manual workloads and improve turnaround times.

- Customer expectations: Real-time decisions, faster onboarding and personalization are now only baseline expectations.

As agentic AI in banking 2026 evolves, the shift is no longer just experimental. Agentic AI use cases in banking are becoming essential for managing risk, improving efficiency and staying competitive in a rapidly evolving landscape.

How is Agentic AI Different From Traditional Banking Automation Systems?

It’s important to understand how agentic AI in banking differs from traditional rule-based automation and chatbot systems already used in banks today. The key difference lies in moving from instruction-following systems to goal-driven execution.

| Aspect | Traditional Banking Automation | Agentic AI in Banking |

| Autonomy | Works within fixed rules and predefined workflows, reacting only when triggered. | Operates with clear goals and decides the best steps to achieve them independently. |

| Integration | Functions as isolated tools across specific banking processes. | Connects and coordinates across multiple systems end-to-end. |

| Context Handling | Treats each interaction separately without memory of past actions. | Maintains context across sessions, channels and workflows. |

| Execution Ability | Primarily suggests actions or automates small repetitive tasks. | Can execute full workflows like fraud checks, alerts, or transaction handling. |

| Adaptability | Needs manual updates or reprogramming for new scenarios. | Learns from outcomes and adapts to changing patterns over time. |

This shift is what defines modern agentic AI use cases in banking, systems that don’t just support decisions but actively carry them out across complex banking operations.

Key Features of a Secure and Scalable Agentic AI System in Banking

Agentic AI in banking only delivers value at scale when it is built with strong controls, deep system integration and regulatory alignment. Systems like those built at Dextralabs are designed to operate autonomously while still staying fully compliant with banking policies and regulations.

1. Controlled Autonomy with Clear Guardrails

Agentic systems are goal-driven but operate within defined banking rules. Every action is constrained by compliance policies, risk limits and approval conditions to ensure safe execution.

2. Security Built Into Every Layer

In AI agents in banking, security is embedded across identity access, encryption, audit trails and monitoring. This ensures every decision and action remains traceable and verifiable for regulatory audits.

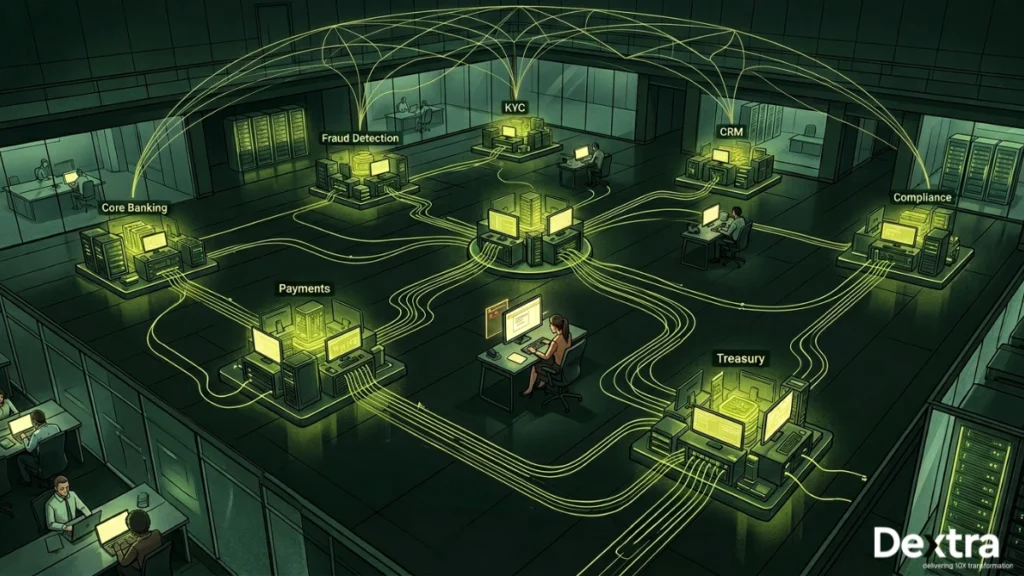

3. End-to-End System Integration

Unlike isolated automation tools, agentic systems connect core banking platforms such as loan management, CRM, fraud detection and payments. This enables complete workflow execution instead of fragmented tasks.

4. Pre-Execution Validation for High-Risk Actions

Critical actions like approvals or fund transfers go through validation or simulation steps before execution. This reduces errors and ensures alignment with internal policies.

5. Continuous Context Awareness

The system maintains context across customer interactions, transactions and channels. This improves decision consistency across agentic AI use cases in banking, especially in lending, onboarding and fraud detection.

6. Scalable Cloud-Native Architecture

Dextralabs builds agentic AI systems on modular, cloud-based infrastructure. This allows banks to scale operations efficiently without replacing existing legacy systems, making it suitable for agentic AI in banking 2026 deployments.

Top 7 Agentic AI Use Cases in Banking in 2026

Agentic AI is already reshaping core banking workflows by shifting from supportive tools to systems that actively participate in decisions and execution. The use cases below highlight where AI agents in banking are delivering the most visible impact across operations, risk and customer experience.

1. Fraud Detection and Transaction Monitoring

Agentic systems continuously monitor transactions, flag anomalies and trigger preventive actions in real time. Unlike rule-based systems, they adapt to new fraud patterns without manual updates.

Dextralabs’ Fraud Monitoring AI Agent operationalizes this by combining real-time event processing with behavioral analysis and risk scoring models. It continuously learns from transaction patterns, feedback loops and historical fraud cases to improve detection accuracy over time.

Example: A suspicious cross-border transfer is automatically blocked, investigated and escalated with a full risk summary. Dextralabs has implemented similar real-time monitoring workflows that reduce fraud response time significantly in production environments.

2. KYC and Customer Onboarding

Onboarding workflows are automated end-to-end, from document verification to risk scoring and account activation. This reduces onboarding time while improving compliance accuracy.

A KYC Automation AI Agent coordinates these steps across systems, handling document parsing, identity validation and sanctions screening in a single workflow. It also manages exceptions, flags inconsistencies and maintains a complete audit trail for compliance and internal review.

Example: At Dextra Labs, a customer came with a customer onboarding issue. So we created a kyc automation AI agent that submits ID documents and the system validates identity, checks sanctions lists and also opens the account within minutes.

3. Credit Underwriting and Loan Processing

Loan decisions are increasingly driven by systems that evaluate income, credit history and risk signals in real time. This reduces dependency on manual underwriting teams.

A Credit Decisioning Agent operationalizes this by applying risk models, policy rules and alternative data sources to generate consistent decisions. It also captures decision logic for explainability and routes edge cases for manual review when needed.

Example: A small business applies for a loan during peak processing hours, where manual underwriting would typically delay decisions by days. Dextra Labs’ credit decisioning agent evaluates income data, transaction behavior and alternative risk signals in real time to generate an approval decision. Edge cases are automatically routed for human review with full explainability, reducing decision time from days to minutes while maintaining compliance.

4. Compliance Monitoring and Regulatory Reporting

Compliance workflows run continuously in the background, tracking transactions and generating audit-ready reports. This reduces manual compliance effort and improves accuracy.

Dextra Labs’ Compliance Monitoring AI Agent ensures this happens reliably by mapping activities to regulatory requirements, detecting anomalies and generating structured reports with full traceability. It also adapts to regulatory updates without requiring constant manual intervention.

Example: Dextra Labs offer a compliance monitoring agent that continuously scans transactions, flags anomalies and generates audit-ready reports. Suspicious activity reports are auto-created and submitted in real time, reducing manual compliance effort and delays.

5. Customer Service and Engagement

Customer service agents operate as real-time orchestration systems that sit on top of banking APIs and core transaction systems.

When a customer query is received, a natural language understanding layer extracts intent, customer context and required action. The system then queries backend services such as payments, account management and transaction systems through secure APIs.

A context management layer maintains conversation history across channels, allowing the agent to continue workflows without losing state. If the confidence score drops or the request requires policy exceptions, the system automatically escalates the case to a human agent with full context and transaction history attached.

A Customer Support Agent supports this by integrating with backend systems to retrieve data, execute actions and maintain context across conversations.

Example: A failed payment query is resolved instantly by Dextra Labs’ customer support agent, which retrieves transaction data, identifies the issue and triggers a refund workflow within the same interaction.

6. Treasury and Cash Management

Treasury agents operate as real-time liquidity monitoring and forecasting systems connected to internal banking ledgers and external market data sources.

They continuously ingest cash inflows, outflows and interbank positions into a liquidity modeling engine, which calculates current exposure and projected cash positions.

A forecasting layer uses time-series models to predict liquidity gaps and recommend fund reallocations across accounts or instruments. Alerts are triggered when thresholds are breached and suggested actions are routed to treasury dashboards or execution systems.

A Treasury Intelligence Agent enables this by providing real-time visibility into cash positions, forecasting liquidity needs and recommending fund allocation strategies.

Example: A bank treasury desk receives real-time alerts for liquidity gaps along with recommended fund reallocations. Dextra Labs builds workflow-driven treasury systems that help financial teams reduce manual coordination and improve cash management efficiency.

7. Frontline Sales and Relationship Management

Relationship intelligence agents function as behavioral analytics + recommendation systems embedded into CRM and banking data layers.

They continuously ingest data from transaction systems, product usage logs, engagement history and lifecycle events. This data is processed through a feature aggregation layer, which builds a real-time customer profile.

A recommendation engine then applies propensity models to identify cross-sell and upsell opportunities. These insights are pushed directly into CRM workflows, enabling relationship managers to act in real time.

A Relationship Intelligence Agent delivers these insights by analyzing transaction patterns, engagement history and lifecycle signals.

Example: Dextra Labs’ relationship intelligence agent analyzes customer behavior and transaction history to recommend the next-best product, enabling timely cross-sell opportunities and improved engagement.

How to Implement Agentic AI in Banking: Dextra Labs 4-Step Execution Framework

This is the structured approach we follow at Dextra Labs to implement agentic AI in banking, ensuring a smooth transition from pilot to production.

It is designed to deliver early results, maintain regulatory alignment and scale reliably within complex banking environments.

Phase 1: Opportunity Assessment and Pilot Design (Weeks 1–4)

The implementation begins with a structured assessment of the bank’s operations to determine where automation will deliver the highest impact. Instead of starting with a broad transformation agenda, we focus on selecting well-defined, data-ready processes that can produce measurable outcomes quickly.

At Dextralabs, we map workflows end-to-end, identify bottlenecks and evaluate data readiness, system dependencies and business impact. Based on this analysis, we recommend the most suitable domains for an initial pilot, whether it is KYC processing, reconciliation workflows, compliance reporting, or more complex areas depending on the organization’s readiness.

What sets Dextralabs apart is our focus on execution readiness. We quantify each use case with clear success metrics, define the technical approach and design the pilot architecture upfront to ensure seamless integration and scalability.

The pilot is executed by a focused team consisting of a product owner, data engineer and AI engineers, ensuring speed without compromising on technical depth or scalability.

Phase 2: Agent Development and Integration (Weeks 5–12)

Once the use case is finalized, the agent is built using a structured four-layer architecture covering reasoning, tool usage, memory and execution control. The system is integrated directly into banking infrastructure through secure APIs.

A critical part of this phase is data readiness. In most banking environments, data is fragmented across legacy systems, making preparation and structuring essential for reliable execution. A substantial effort is required to clean, integrate and organize data through reliable pipelines before it can support consistent outcomes.

Guardrails and escalation logic are embedded from the beginning to ensure safe execution within regulatory and internal policy boundaries.

Phase 3: Supervised Deployment (Weeks 13–16)

The agent is deployed in a co-pilot mode where it executes workflows but every action is reviewed before final execution. This allows banks to validate performance in real operational environments without risk exposure.

Key metrics such as processing time, accuracy, escalation rate and false positives are continuously tracked and benchmarked against existing processes to ensure reliability and performance before increasing autonomy.

Phase 4: Autonomous Scaling (Weeks 17–24)

Once the system demonstrates stable performance, autonomy is gradually increased based on confidence scoring. High-confidence actions are executed automatically, while low-confidence cases are escalated for human review.

Scaling is done carefully, first within the same workflow category, then expanded into adjacent processes. This controlled approach ensures stability while enabling broader adoption of agentic AI in banking and financial services.

This final phase enables a controlled shift from pilot-level autonomy to full production deployment across banking environments.

From Pilot to Production at Scale

This phased approach is how we structure every banking engagement at Dextra Labs. It ensures a smooth progression from a single-domain pilot to coordinated multi-agent deployment across compliance, onboarding and operations, without introducing operational disruption.

If you’re evaluating where to start, our team can help identify the highest-ROI domain for your first deployment and define a clear path to scale.

You can explore real-world implementations and outcomes in our AI agent development services here.

Benefits of Agentic AI in Banking and Financial Services

Agentic AI in banking goes beyond generating insights. It connects systems, decisions and actions that are usually spread across different teams and platforms. This helps reduce delays and removes much of the operational friction seen in traditional banking workflows. Let’s look at some other benefits as well!

1. Unifies Fragmented Banking Systems into One Flow

Most banks still operate with separate platforms for risk, compliance, CRM and core banking. Agentic systems bring these together so information and actions can move seamlessly across workflows.

- Pulls data from core banking, AML, CRM and external systems

- Automatically triggers next steps instead of stopping at alerts

- Reduces dependency on manual coordination between teams

2. Speeds Up Decision and Action Cycles

Instead of waiting for human review at every single step, routine decisions can move forward instantly within defined rules. This significantly reduces turnaround time across key banking processes.

- Faster approvals in onboarding, lending and compliance checks

- Immediate response to triggered events or alerts

- Reduced delays caused by handoffs between teams

3. Reduces Manual Workload Across Operations

A large part of banking operations still involves repetitive checks, validations and follow-ups. These can be handled directly within automated workflows, freeing teams for higher-value tasks.

- Automates repetitive operational and verification tasks

- Minimizes manual data handling and entry work

- Improves overall team productivity

4. Improves Accuracy and Reduces Operational Errors

Human-driven processes often lead to inconsistencies, especially at scale. Structured execution reduces errors and ensures consistent outcomes across workflows.

- Standardizes decision-making across processes

- Reduces errors in data handling and approvals

- Ensures consistent application of banking rules

5. Strengthens Compliance and Audit Readiness

Regulatory checks become continuous rather than periodic. Every action is tracked, making audits and reporting more transparent and reliable.

- Maintains real-time logs of decisions and actions

- Flags compliance issues as they happen

- Simplifies audit preparation and reporting cycles

6. Enhances Customer Experience

Faster processing and fewer handoffs directly improve how customers experience banking services. Queries and requests are resolved with less waiting time and better accuracy.

- Faster onboarding and issue resolution

- More consistent communication across channels

- Reduced delays in service requests

7. Better Risk Visibility Across Operations

Agentic systems continuously track transactions and behaviors across multiple systems, giving banks a clearer and more connected view of risk. This helps identify issues earlier instead of reacting after damage is done.

- Combines signals from multiple data sources for better risk context

- Detects unusual patterns in real time

- Helps teams act before risks escalate

8. More Efficient Loan and Credit Workflows

Loan processing becomes faster and more consistent when financial data, credit history and risk checks are handled in one connected flow. This reduces bottlenecks in underwriting and approval cycles.

- Automates credit evaluation and documentation checks

- Speeds up loan approvals and disbursements

- Reduces dependency on manual underwriting reviews

9. Smarter Use of Banking Data

Banks generate large volumes of data, but much of it remains underused. Agentic systems help convert this data into actionable steps across different workflows.

- Connects structured and unstructured data sources

- Uses real-time insights to guide decisions

- Reduces reliance on static reports

10. Scalable Operations Without Linear Cost Growth

As transaction volumes increase, traditional systems require more staff as well as effort. Agentic systems scale operations without a proportional increase in manual workload.

- Handles higher volumes without adding equivalent headcount

- Supports expansion across multiple banking functions

- Improves operational efficiency at scale

“Most banks don’t fail at AI because of models. They fail because systems don’t integrate, data isn’t ready and execution breaks between teams.” – Dextra Labs’ CTO

4 Barriers to Adoption of Agentic AI in Banking

Despite strong momentum, agentic AI in banking is still difficult to scale in real-world environments. Most large banks face structural, regulatory as well as organizational challenges that slow down adoption and limit full-scale deployment.

1. Legacy Core System Constraints

Most banks still rely on core banking systems that were built 20–40 years ago, which were not designed for API-driven or real-time agent interactions. This creates integration challenges across workflows.

Data is often spread across disconnected front-office, back-office and risk systems, making it difficult for agents to get a complete view of operations.

2. Evolving Regulatory Expectations

Regulation around AI in banking is still developing, especially around transparency and explainability. From 2026, the EU AI Act requires financial systems to clearly explain decision-making processes, not just outputs.

This means banks need systems that can justify every action taken, which adds complexity to agentic AI in banking use cases.

3. Poor Data Quality and Fragmentation

Agent performance depends heavily on the quality of underlying data. In many banks, data remains fragmented across multiple systems and formats, limiting reliability and speed.

Banks with unified data infrastructure see significantly better performance, while others spend a large share of their effort just cleaning and connecting data pipelines.

4. Organizational and Skill Gaps

A major challenge is not technical but organizational. Around 62% of banks report a shortage of AI and data engineering skills needed to manage these systems.

The shift from manual execution to supervising intelligent systems also requires new roles, updated workflows and cultural change across teams. This is where AI consulting expertise bridges the gap between what banks want to build and what their current teams can execute.

Why Dextra Labs is the Best Partner to Build Agentic AI Systems in Banking?

Most financial institutions don’t struggle with AI because of models. They struggle with execution.

In many banking environments, AI systems remain stuck in pilot stages because they are built as isolated solutions. They don’t integrate deeply with core banking systems, lack reliable data pipelines and cannot operate within strict regulatory constraints. As a result of this, even promising use cases fail to scale beyond controlled environments.

Dextra Labs approaches this differently by focusing on how agentic systems actually run in production.

Instead of treating AI agents as standalone components, our systems are designed as orchestrated execution layers that sit on top of existing banking infrastructure.

At a system level, this typically involves:

- Separation of Reasoning, Memory and Execution Layers: Decision-making (LLMs), contextual memory (vector databases + session state) and action execution are handled independently to improve control and reliability.

- Orchestration Across Multiple Banking Systems: Agents are connected to core systems such as CRM, loan management, payment gateways and compliance tools through secure APIs and event-driven pipelines, enabling end-to-end workflow execution instead of isolated task automation.

- Built-in Guardrails and Validation Mechanisms: Every action whether it’s a transaction flag, loan approval step, or compliance trigger is governed by predefined policies, confidence thresholds and escalation logic to ensure regulatory alignment.

- Auditability and Traceability by Design: All agent decisions and actions are logged with structured reasoning paths, making them explainable as well as reviewable for internal audits and regulatory requirements.

- Data Readiness and Pipeline Engineering: A significant part of the implementation focuses on cleaning, structuring and connecting fragmented banking data so that agents can operate reliably in real-time environments.

This architecture allows agentic AI systems to move beyond pilot use cases and operate reliably across high-volume, high-risk banking workflows such as KYC/AML, fraud monitoring, loan processing and reconciliation.

The result is not just automation, but coordinated execution across systems, where decisions and actions happen within the same workflow, rather than across disconnected tools and teams.

Conclusion

Agentic AI in banking has already moved beyond experimentation into real production at scale in 2026. The gap between early adopters and slower movers is widening, with leading banks already seeing significant cost savings and improvements in revenue, while others are still stuck in pilot projects with limited scale.

Dextra Labs builds custom agentic AI systems for banks and financial institutions from single-domain pilots to enterprise-wide multi-agent deployments. If you’re evaluating agentic AI for your banking operations, talk to our financial services team.

Frequently Asked Questions (FAQs):

What is the future of verified AI agent payments in banking and ecommerce?

The future of verified AI-driven payments in banking and ecommerce is expected to focus on making transactions faster while maintaining strong security and compliance checks. The goal is to reduce manual approval steps without compromising trust, governance, or regulatory requirements. However, some key shifts that are expected with evolving future, includes the following:

– Faster, near-instant payment processing

– Stronger automated fraud and identity checks

– Reduced friction in checkout and transfers

How does agentic AI enhance customer engagement in banking?

Customer interactions become much smoother because systems remember context and respond faster across channels. This reduces repetition and improves the overall service experience.

How do businesses integrate agentic infrastructure with core banking systems?

Integration is done by connecting existing banking systems so data and actions can move in real time. The goal is to make legacy and modern systems work together without disruption.

Typical approach:

– API-based connection to core banking systems

– Secure data sharing across departments

– Middleware support for legacy platforms

How much does it cost to develop an agentic AI system for a bank?

The cost varies widely based on scope, complexity and integration needs. Most investment goes into data preparation, system integration and security rather than core model development.

How can AI help in banking fraud analytics?

It helps banks detect suspicious activity faster by continuously monitoring transactions and identifying unusual patterns. This reduces reaction time and improves risk control.

Key benefits:

– Real-time fraud detection

– Early identification of abnormal behavior

– Reduced false alerts compared to static rules

How is AI used in banking?

It is used across core banking functions to improve speed and reduce manual effort. The biggest impact is seen in risk, operations and customer service.

How does generative AI improve customer experience in banking?

It simplifies customer interactions by giving faster and more conversational responses. This reduces dependency on long support processes.

Can AI be used for bank reconciliation in Excel?

Yes, it can help automate matching and highlight mismatches in large datasets. This reduces manual spreadsheet work and improves accuracy.